(The Battle of Inflation vs. Interest)

If you are keeping the bulk of your cash in a standard checking account or a “big bank” savings account, you might feel safe. The number on the screen isn’t going down, right?

Unfortunately, that isn’t the whole story. While the number remains the same, the value of that money is quietly shrinking every single day.

This is the silent erosion of wealth caused by the gap between Inflation and Interest. Here is why your checking account is costing you money, and why a High-Yield Savings Account (HYSA) is the easiest financial win you can make today.

The Silent Thief: Inflation

Inflation is the rate at which the cost of goods and services rises over time. If inflation is hovering around 3%, a gallon of milk that costs $4.00 today will effectively cost $4.12 next year.

To break even, your money needs to grow at the same pace as inflation.

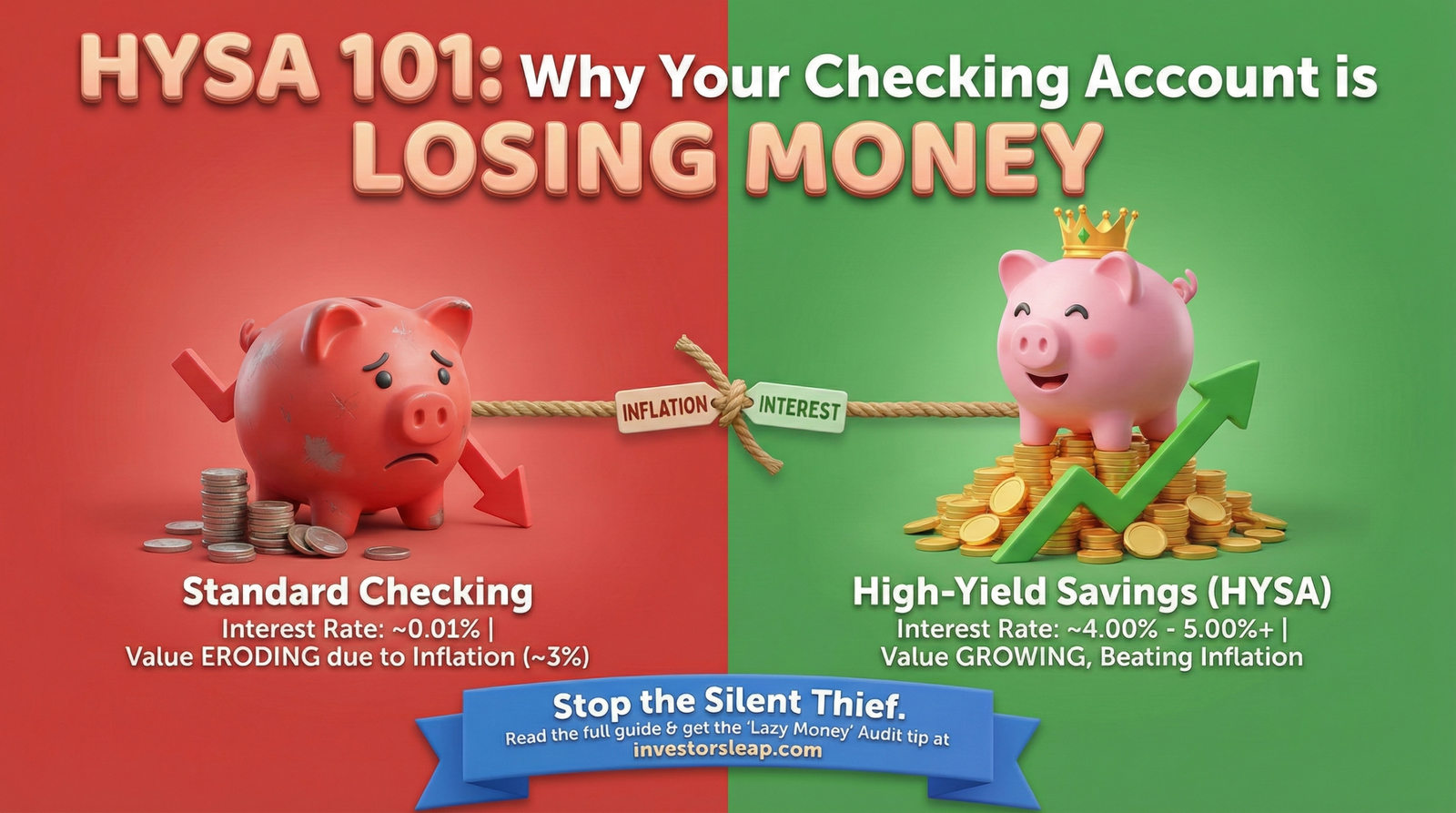

- The Reality: Most standard checking accounts pay an interest rate of 0.01% (or nothing at all).

- The Math: If inflation is 3% and your bank pays 0.01%, your “Real Rate of Return” is roughly -2.99%.

The Example:

Imagine you have $10,000 sitting in a standard checking account for one year.

- Interest Earned: $1.00

- Purchasing Power Lost (due to 3% inflation): ~$300.00

You didn’t spend a dime, but you are effectively $299 poorer in terms of what you can actually buy.

The Solution: The High-Yield Savings Account (HYSA)

A High-Yield Savings Account is exactly what it sounds like: a savings account that pays a significantly higher interest rate than national averages—often 10x to 20x higher.

Why do they pay so much more?

These accounts are typically offered by online-only banks. Because they don’t have to pay for thousands of brick-and-mortar branches, tellers, or expensive real estate, they pass those savings on to you in the form of higher Annual Percentage Yields (APY).

The HYSA Difference:

Let’s look at that same $10,000 in an HYSA paying 4.5% APY.

- Interest Earned: $450.00

- Purchasing Power: You have outpaced (or at least kept up with) inflation.

Instead of losing value, your emergency fund or down payment savings is now generating enough cash to pay for a utility bill or a nice dinner out, simply by sitting in a different digital bucket.

Common Myths About HYSAs

If you haven’t switched yet, it’s usually because of one of these three fears. Let’s debunk them:

- “Is my money safe?”Yes. Legitimate HYSAs are FDIC Insured (typically up to $250,000 per depositor), just like your checking account at a major bank. If the bank fails, the government protects your money.

- “Is my money locked up?”No. Unlike a Certificate of Deposit (CD), your money is liquid. You can transfer it back to your checking account whenever you need it, usually within 1-2 business days.

- “Is it hard to switch?”It takes about 10 minutes. You link your current checking account, transfer the funds, and you’re done.

Comparison at a Glance

| Feature | Standard Checking | High-Yield Savings (HYSA) |

| Interest Rate (APY) | ~0.01% | ~4.00% – 5.00%+ |

| Fees | Often has monthly maintenance fees | Usually $0 monthly fees |

| Access | Instant (Debit Card/ATM) | 1-3 Days (Transfer required) |

| Best For | Paying bills, daily spending | Emergency fund, travel fund, house down payment |

🚀 InvestorsLeap Tip: The “Lazy Money” Audit

Don’t let your money be lazy. We recommend keeping 1 to 2 months of expenses in your checking account for immediate cash flow needs.

Everything else—your 3-6 month emergency fund, your vacation savings, or cash waiting to be invested—should be moved immediately to an HYSA. Every day those funds sit in checking is a day you are voluntarily donating purchasing power to inflation.

Make your money work as hard as you do.

{kind=link}